Blog

Our blogs focus on AAVUL's many wealth and investment planning applications.

Identifying Advice Is Powerful Differentiation

Advice options have proliferated for the investor marketplace. Broker-dealers, independent RIAs, banks, insurance companies, and accounting firms all offer planning/investment advisory in one form or another. Add to that the rush of Robo-Advisor options, and it’s clear that the retail market has more choice in firms offering planning/investment advisory services than ever before.

Commoditization

A commodity is a product or service indistinguishable in features and functions. Where does commoditization exist in the adviser market?

- Services. Advisers of all types offer a service set that includes these categories: financial planning, portfolio building, investment selection, reporting, and monitoring.

- Service Output. If adviser “A” and adviser “B” use the same software tools, the packaging, presentation, and content will be within a narrowly-defined range.

- Investment Products. The failure of active management to produce persistent alpha (The New York Times) has pushed passive and other quantitative investment strategies to leadership (Investment News); ETFs have become the vehicle of choice (FPA investing study).

- Credentials. It’s difficult for a client/investor to appreciate the practical differences between designations such as a CFP®, ChFC, PFS, and CIMA.

- Pricing. A percentage fee on AUM remains the dominant structure.

Once commoditization begins, it’s rare that it stops. This is largely due to the consuming market’s demands. In other words, for a firm to be taken seriously, consumers expect certain features at a minimum, and, as one solution adds a new feature, competitors’ quick response relegates the erstwhile new feature to commodity status (and the market’s base-level expectation rises). This relentless “me-tooism” leads non-responsive firms to obsolescence.

Differentiating the Product through Design and Engineering

It’s common across all industries to find competitors with commodity-like elements inside a product or in delivery. For example, a manufacturer of a computer, a TV, or a car use the same raw materials and, often, the same suppliers. Car manufacturers all use dealers for sales and service. What drives a manufacturer’s marketing focus is not parts and subassemblies, but the product’s design and engineering.

An Adviser Designs and Engineers with Advice/Counsel/Wisdom

A lot of worthy time is spent refining an advisory firm’s web presence, staff, client service, and technology. These are all important tactics, but they will miss the mark if this core reality is ignored: in a professional services business, the practitioner is hired for—and defined by—his or her advice/counsel/wisdom.

It is this advice—the practitioner’s essence—that designs and engineers the product and service solution. Marketing the evidence of this advice raises it to be a true differentiating beacon.

Spotlight the Presence of Advice/Counsel/Wisdom

It’s incorrect to assume that prospects and clients readily see or understand how an adviser’s advice/counsel/wisdom was used to develop and execute a wealth plan. Since advice is central to an adviser’s value proposition, at each step where analytical and creative advice was used, explicit identification spotlights its application.

Verbal Markers. “From what you’ve told me here, your anxiety in having enough money brings to the forefront our portfolio designs that produce secure income. Here’s how it works . . . [i.e. defining the advice/counsel/wisdom]”

Written Markers. “Your desire to protect what you’ve earned is designed into our tax management and wealth protection program. As we illustrate below . . . [i.e. defining the advice/counsel/wisdom]”

Naming Investment Philosophies, Designs, and Approaches

A wealth manager’s execution tools include investment products (e.g. ETFs, mutual funds, etc.), insurance products, tax strategies, trusts, and the like. How an adviser integrates these tools into wealth solutions is a direct result of advice/counsel/wisdom. Naming or branding all such approaches solidifies, competitively, advice differentiation.

For example, if an adviser has an approach for wealth protection that combines low volatility investments and insurance products, the firm can brand it with a name such as “[firm name] Wealth Guardian.” The naming/branding step elevates the advice/counsel/wisdom into a definable component; it moves from concept to function.

Case Studies (Stories) for Marketing

Client stories or case studies bring advice alive to prospects not yet able to experience it directly. Indeed, illustrating how advice/counsel/wisdom has brought added value to others is the ultimate differentiation message; this can be done in one-page marketing slip sheets that memorialize the power of advice in action.

Being Clear Amidst the Fog

The wealth management process is fogged with a client’s background, memories, values, beliefs, needs, anxieties, and aspirations. In the presence of this fog, explicit identification of the practitioner’s design and engineering prowess acts as a beacon directing the client to the adviser’s differentiating value—his or her advice/counsel/wisdom.

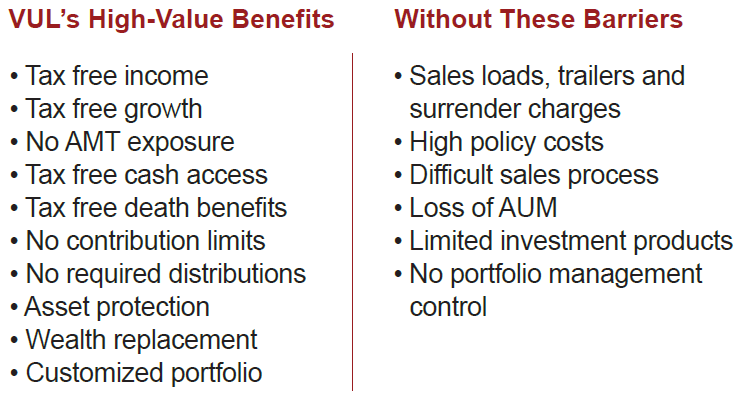

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.