AAVUL’s Call to the Fiduciary Advisor

Blog

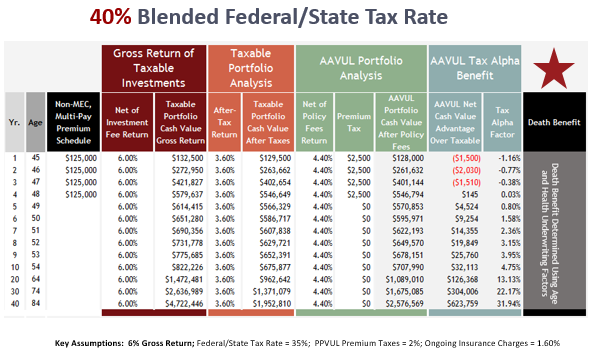

Our blogs focus on AAVUL's many wealth and investment planning applications.

Insurance: A Force Underpinning the Global Economy

In various surveys asking people about the greatest inventions of all time, electricity, clean water, penicillin, engines, and the internet came out ahead.

Insurance didn’t make the list.

In fact, one of the core foundations that allows the global economy to function efficiently is risk sharing, the concept defining insurance. Whether it be companies or individuals, knowing that catastrophic financial loss is protected enlivens risk taking while undergirding a willingness to commit investment capital. Many of the top product inventions would not have made it from the lab to production and into people’s hands if insurance didn’t exist.

Insurance allows people – individuals or business leaders – to proceed confidently in the face of an uncertain future. Because insurance (risk sharing) is so vital, most developed countries enact laws that make insurance either favorable financially (life) or mandatory (auto).

Knowing that valuable financial assets and human resources are protected facilitates the free flow of capital in the form of bank loans, bonds, and equity.

With individuals, protecting property and lives through insurance brings peace of mind that otherwise would be lost, if, for example, financial ruin resulted from a car accident, home fire, illness, or a breadwinner’s death.

Insurance: A Bad Reputation

One would think that insurance’s importance as a financial bulwark and peace-giver would elicit good feelings, but that isn’t the usual case. Studies repeatedly reveal that insurance products have bad reputations as too complex, too costly, and too pushy.

This is not a malady for the concept of insurance, but how it has historically been designed, marketed, sold, and serviced. Private wealth advisors are not immune to having had bad insurance product experiences.

No advisor would deny how important insurance is to a client’s financial security, but, commonly, there’s friction to a welcome embrace. This friction arises from three main sources:

1. Complexity

The way insurance products are designed and executed brings unnecessary complexity. While consumers are often flummoxed, these same people hire advisors to be experts in their place.

This brings fee-only advisors a day-to-day challenge along with a business risk. First, it takes time – a precious commodity for a service provider – to become an expert in insurance products’ fine print. Second, advisors face this complexity with an even bigger burden: if a complex insurance product is misunderstood and then misapplied, the client could be hurt financially and damage the advisor’s relationship.

2. Competing Voices

Selling life insurance products requires a license to do so. In most insurance company distribution models, this required “ticket to the game” allows an agent to have a seat at the client’s table for each insurance product transaction.

Meanwhile, agents (especially life insurance) with a seat at the transaction table increasingly are expanding their own services to include financial planning and investment programs. For the fee-only advisor, this expansion represents a potentially unwelcome, competing voice of thoughts and plans within the client relationship.

3. Conflicting Interests

The common compensation method for insurance products is a sales commission.

All transaction-based compensation methods tempt a seller to seek his or her own financial self-interest instead of the buyer’s best interest.

The fiduciary standard – seeking the client’s best interest in all circumstances – is a cornerstone of the fee-only advisor. Mixed compensation methods in an advisory relationship open the door to both confusion and conflict, producing hesitancy with the fee-only advisor (the one with the most to lose in a bad outcome).

Insurance: Applied to the Fiduciary Standard

For some fee-only advisors, bad insurance product experiences may lead to an expressed “not for me” attitude whereas others may react more subconsciously, but with the same biased reluctance.

The fiduciary standard’s best-interest call is not static. Indeed, fiduciary advisors are compelled to periodically put product biases (for and against) under a spotlight and learn with an open mind. These due diligence questions should be asked in every advisory firms’ investment committee at least twice a year when considering investment performance:

- “What new investment products have emerged that fit with our clients’ needs?”

- “Have certain investment product fees changed to make investing more efficient?”

- “How can wealth be better protected?”

Adhering to the fiduciary standard pushes advisors to continually rethink and recalibrate. For example, ETFs forced fee-only advisors to reconsider their mutual fund devotion. Now, advisors liberally allocate assets to ETFs, sometimes even to the exclusion of mutual funds.

The fiduciary standard is a prevailing call to stay current with planning and investment innovation. From new investment categories to rebalancing practices to practice management methods, an advisory firm’s willingness to innovate sets the stage for long-term growth.

Insurance: Innovation for the Fee-Only Advisor

Even though the DOL’s proposed fiduciary standard is a political football, it has enlivened insurance product development to align insurance benefits to the fee-only advisor’s fiduciary standard. (Note: many fee-only insurance products have been in the market for years, but often under the radar of the private wealth advisor; the DOL’s fiduciary rule initiative brought the importance of “best interest” insurance products into the limelight.)

These products (primarily annuities and life insurance) provide five essential functions:

- Strip away transaction-based compensation

- Remove complex fee structures

- Provide an external salaried agent/partner to execute the transaction

- Place the fee-only advisor as the overseer of the wealth inside the insurance product

- Keep the advisor in charge of the client relationship

Indeed, with fee-only variable annuities and variable universal life products (responsive to the fiduciary standard), the advisor stays in the essential role as the builder, manager, and monitor of the products’ underlying portfolios. This keeps an insurance product’s invested wealth fully integrated in the client’s wealth and investment plans.

The advisor gains an essential investment resource, the client gains peace of mind (and a highly tax-advantaged investment experience), and innovation reveals itself in the wealth plan.

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

The new Advisor-Applied VUL.

It’s low-cost, one-step tax alpha.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.

“Invest for maximum total REAL return. This means the return on invested dollars after taxes and after inflation. This is the only rational objective for most long-term investors. Any investment strategy that fails to recognize the insidious effect of taxes and inflation fails to recognize the true nature of the investment environment and thus is severely handicapped.” John Templeton

“Invest for maximum total REAL return. This means the return on invested dollars after taxes and after inflation. This is the only rational objective for most long-term investors. Any investment strategy that fails to recognize the insidious effect of taxes and inflation fails to recognize the true nature of the investment environment and thus is severely handicapped.” John Templeton

Recent Comments