Your Firm’s Investment Products; The AAVUL Fit

Use your existing fund structure (no IDF) to include private wealth clients investing through AAVUL.

TAX FREE FOR ALL:

Private Wealth Like an Institution

“AAVUL, with its tax-free and open architecture investing structure, offers private investment firms – especially hedge fund, real estate, and private equity strategies – a simplified path to increased after-tax performance for private wealth clients.”

CALCULATE IT:

Projected Tax Savings to Your Products’ Return

Check out the tax-free potential of your firm’s investment products inside AAVUL.

The Tax Shield Ratio Calculator identifies if your firm’s investment products’ return profile, combined with a private wealth client’s tax rate and policy expenses, will produce more client profits inside the policy than keeping the client’s investment in a taxable portfolio.

Tax Shield Ratio (TSR) Calculator

Inputs

Results

| Blended Federal and State Tax Rate | Pre-Tax Rate of Return | Blended Federal and State Tax Rate | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1% | 2% | 3% | 4% | 5% | 6% | 7% | 8% | 9% | 10% | 11% | 12% | 13% | 14% | 15% | 16% | 17% | 18% | 19% | 20% | ||

| 15% | 0.15 | 0.30 | 0.45 | 0.60 | 0.75 | 0.90 | 1.05 | 1.20 | 1.35 | 1.50 | 1.65 | 1.80 | 1.95 | 2.10 | 2.25 | 2.40 | 2.55 | 2.70 | 2.85 | 3.00 | 15% |

| 16% | 0.16 | 0.32 | 0.48 | 0.64 | 0.80 | 0.96 | 1.12 | 1.28 | 1.44 | 1.60 | 1.76 | 1.92 | 2.08 | 2.24 | 2.40 | 2.56 | 2.72 | 2.88 | 3.04 | 3.20 | 16% |

| 17% | 0.17 | 0.34 | 0.51 | 0.68 | 0.85 | 1.02 | 1.19 | 1.36 | 1.53 | 1.70 | 1.87 | 2.04 | 2.21 | 2.38 | 2.55 | 2.72 | 2.89 | 3.06 | 3.23 | 3.40 | 17% |

| 18% | 0.18 | 0.36 | 0.54 | 0.72 | 0.90 | 1.08 | 1.26 | 1.44 | 1.62 | 1.80 | 1.98 | 2.16 | 2.34 | 2.52 | 2.70 | 2.88 | 3.06 | 3.24 | 3.42 | 3.60 | 18% |

| 19% | 0.19 | 0.38 | 0.57 | 0.76 | 0.95 | 1.14 | 1.33 | 1.52 | 1.71 | 1.90 | 2.09 | 2.28 | 2.47 | 2.66 | 2.85 | 3.04 | 3.23 | 3.42 | 3.61 | 3.80 | 19% |

| 20% | 0.20 | 0.40 | 0.60 | 0.80 | 1.00 | 1.20 | 1.40 | 1.60 | 1.80 | 2.00 | 2.20 | 2.40 | 2.60 | 2.80 | 3.00 | 3.20 | 3.40 | 3.60 | 3.80 | 4.00 | 20% |

| 21% | 0.21 | 0.42 | 0.63 | 0.84 | 1.05 | 1.26 | 1.47 | 1.68 | 1.89 | 2.10 | 2.31 | 2.52 | 2.73 | 2.94 | 3.15 | 3.36 | 3.57 | 3.78 | 3.99 | 4.20 | 21% |

| 22% | 0.22 | 0.44 | 0.66 | 0.88 | 1.10 | 1.32 | 1.54 | 1.76 | 1.98 | 2.20 | 2.42 | 2.64 | 2.86 | 3.08 | 3.30 | 3.52 | 3.74 | 3.96 | 4.18 | 4.40 | 22% |

| 23% | 0.23 | 0.46 | 0.69 | 0.92 | 1.15 | 1.38 | 1.61 | 1.84 | 2.07 | 2.30 | 2.53 | 2.76 | 2.99 | 3.22 | 3.45 | 3.68 | 3.91 | 4.14 | 4.37 | 4.60 | 23% |

| 24% | 0.24 | 0.48 | 0.72 | 0.96 | 1.20 | 1.44 | 1.68 | 1.92 | 2.16 | 2.40 | 2.64 | 2.88 | 3.12 | 3.36 | 3.60 | 3.84 | 4.08 | 4.32 | 4.56 | 4.80 | 24% |

| 25% | 0.25 | 0.50 | 0.75 | 1.00 | 1.25 | 1.50 | 1.75 | 2.00 | 2.25 | 2.50 | 2.75 | 3.00 | 3.25 | 3.50 | 3.75 | 4.00 | 4.25 | 4.50 | 4.75 | 5.00 | 25% |

| 26% | 0.26 | 0.52 | 0.78 | 1.04 | 1.30 | 1.56 | 1.82 | 2.08 | 2.34 | 2.60 | 2.86 | 3.12 | 3.38 | 3.64 | 3.90 | 4.16 | 4.42 | 4.68 | 4.94 | 5.20 | 26% |

| 27% | 0.27 | 0.54 | 0.81 | 1.08 | 1.35 | 1.62 | 1.89 | 2.16 | 2.43 | 2.70 | 2.97 | 3.24 | 3.51 | 3.78 | 4.05 | 4.32 | 4.59 | 4.86 | 5.13 | 5.40 | 27% |

| 28% | 0.28 | 0.56 | 0.84 | 1.12 | 1.40 | 1.68 | 1.96 | 2.24 | 2.52 | 2.80 | 3.08 | 3.36 | 3.64 | 3.92 | 4.20 | 4.48 | 4.76 | 5.04 | 5.32 | 5.60 | 28% |

| 29% | 0.29 | 0.58 | 0.87 | 1.16 | 1.45 | 1.74 | 2.03 | 2.32 | 2.61 | 2.90 | 3.19 | 3.48 | 3.77 | 4.06 | 4.35 | 4.64 | 4.93 | 5.22 | 5.51 | 5.80 | 29% |

| 30% | 0.30 | 0.60 | 0.90 | 1.20 | 1.50 | 1.80 | 2.10 | 2.40 | 2.70 | 3.00 | 3.30 | 3.60 | 3.90 | 4.20 | 4.50 | 4.80 | 5.10 | 5.40 | 5.70 | 6.00 | 30% |

| 31% | 0.31 | 0.62 | 0.93 | 1.24 | 1.55 | 1.86 | 2.17 | 2.48 | 2.79 | 3.10 | 3.41 | 3.72 | 4.03 | 4.34 | 4.65 | 4.96 | 5.27 | 5.58 | 5.89 | 6.20 | 31% |

| 32% | 0.32 | 0.64 | 0.96 | 1.28 | 1.60 | 1.92 | 2.24 | 2.56 | 2.88 | 3.20 | 3.52 | 3.84 | 4.16 | 4.48 | 4.80 | 5.12 | 5.44 | 5.76 | 6.08 | 6.40 | 32% |

| 33% | 0.33 | 0.66 | 0.99 | 1.32 | 1.65 | 1.98 | 2.31 | 2.64 | 2.97 | 3.30 | 3.63 | 3.96 | 4.29 | 4.62 | 4.95 | 5.28 | 5.61 | 5.94 | 6.27 | 6.60 | 33% |

| 34% | 0.34 | 0.68 | 1.02 | 1.36 | 1.70 | 2.04 | 2.38 | 2.72 | 3.06 | 3.40 | 3.74 | 4.08 | 4.42 | 4.76 | 5.10 | 5.44 | 5.78 | 6.12 | 6.46 | 6.80 | 34% |

| 35% | 0.35 | 0.70 | 1.05 | 1.40 | 1.75 | 2.10 | 2.45 | 2.80 | 3.15 | 3.50 | 3.85 | 4.20 | 4.55 | 4.90 | 5.25 | 5.60 | 5.95 | 6.30 | 6.65 | 7.00 | 35% |

| 36% | 0.36 | 0.72 | 1.08 | 1.44 | 1.80 | 2.16 | 2.52 | 2.88 | 3.24 | 3.60 | 3.96 | 4.32 | 4.68 | 5.04 | 5.40 | 5.76 | 6.12 | 6.48 | 6.84 | 7.20 | 36% |

| 37% | 0.37 | 0.74 | 1.11 | 1.48 | 1.85 | 2.22 | 2.59 | 2.96 | 3.33 | 3.70 | 4.07 | 4.44 | 4.81 | 5.18 | 5.55 | 5.92 | 6.29 | 6.66 | 7.03 | 7.40 | 37% |

| 38% | 0.38 | 0.76 | 1.14 | 1.52 | 1.90 | 2.28 | 2.66 | 3.04 | 3.42 | 3.80 | 4.18 | 4.56 | 4.94 | 5.32 | 5.70 | 6.08 | 6.46 | 6.84 | 7.22 | 7.60 | 38% |

| 39% | 0.39 | 0.78 | 1.17 | 1.56 | 1.95 | 2.34 | 2.73 | 3.12 | 3.51 | 3.90 | 4.29 | 4.68 | 5.07 | 5.46 | 5.85 | 6.24 | 6.63 | 7.02 | 7.41 | 7.80 | 39% |

| 40% | 0.40 | 0.80 | 1.20 | 1.60 | 2.00 | 2.40 | 2.80 | 3.20 | 3.60 | 4.00 | 4.40 | 4.80 | 5.20 | 5.60 | 6.00 | 6.40 | 6.80 | 7.20 | 7.60 | 8.00 | 40% |

| 41% | 0.41 | 0.82 | 1.23 | 1.64 | 2.05 | 2.46 | 2.87 | 3.28 | 3.69 | 4.10 | 4.51 | 4.92 | 5.33 | 5.74 | 6.15 | 6.56 | 6.97 | 7.38 | 7.79 | 8.20 | 41% |

| 42% | 0.42 | 0.84 | 1.26 | 1.68 | 2.10 | 2.52 | 2.94 | 3.36 | 3.78 | 4.20 | 4.62 | 5.04 | 5.46 | 5.88 | 6.30 | 6.72 | 7.14 | 7.56 | 7.98 | 8.40 | 42% |

| 43% | 0.43 | 0.86 | 1.29 | 1.72 | 2.15 | 2.58 | 3.01 | 3.44 | 3.87 | 4.30 | 4.73 | 5.16 | 5.59 | 6.02 | 6.45 | 6.88 | 7.31 | 7.74 | 8.17 | 8.60 | 43% |

| 44% | 0.44 | 0.88 | 1.32 | 1.76 | 2.20 | 2.64 | 3.08 | 3.52 | 3.96 | 4.40 | 4.84 | 5.28 | 5.72 | 6.16 | 6.60 | 7.04 | 7.48 | 7.92 | 8.36 | 8.80 | 44% |

| 45% | 0.45 | 0.90 | 1.35 | 1.80 | 2.25 | 2.70 | 3.15 | 3.60 | 4.05 | 4.50 | 4.95 | 5.40 | 5.85 | 6.30 | 6.75 | 7.20 | 7.65 | 8.10 | 8.55 | 9.00 | 45% |

| 46% | 0.46 | 0.92 | 1.38 | 1.84 | 2.30 | 2.76 | 3.22 | 3.68 | 4.14 | 4.60 | 5.06 | 5.52 | 5.98 | 6.44 | 6.90 | 7.36 | 7.82 | 8.28 | 8.74 | 9.20 | 46% |

| 47% | 0.47 | 0.94 | 1.41 | 1.88 | 2.35 | 2.82 | 3.29 | 3.76 | 4.23 | 4.70 | 5.17 | 5.64 | 6.11 | 6.58 | 7.05 | 7.52 | 7.99 | 8.46 | 8.93 | 9.40 | 47% |

| 48% | 0.48 | 0.96 | 1.44 | 1.92 | 2.40 | 2.88 | 3.36 | 3.84 | 4.32 | 4.80 | 5.28 | 5.76 | 6.24 | 6.72 | 7.20 | 7.68 | 8.16 | 8.64 | 9.12 | 9.60 | 48% |

| 49% | 0.49 | 0.98 | 1.47 | 1.96 | 2.45 | 2.94 | 3.43 | 3.92 | 4.41 | 4.90 | 5.39 | 5.88 | 6.37 | 6.86 | 7.35 | 7.84 | 8.33 | 8.82 | 9.31 | 9.80 | 49% |

| 50% | 0.50 | 1.00 | 1.50 | 2.00 | 2.50 | 3.00 | 3.50 | 4.00 | 4.50 | 5.00 | 5.50 | 6.00 | 6.50 | 7.00 | 7.50 | 8.00 | 8.50 | 9.00 | 9.50 | 10.00 | 50% |

| 51% | 0.51 | 1.02 | 1.53 | 2.04 | 2.55 | 3.06 | 3.57 | 4.08 | 4.59 | 5.10 | 5.61 | 6.12 | 6.63 | 7.14 | 7.65 | 8.16 | 8.67 | 9.18 | 9.69 | 10.20 | 51% |

| 52% | 0.52 | 1.04 | 1.56 | 2.08 | 2.60 | 3.12 | 3.64 | 4.16 | 4.68 | 5.20 | 5.72 | 6.24 | 6.76 | 7.28 | 7.80 | 8.32 | 8.84 | 9.36 | 9.88 | 10.40 | 52% |

| 53% | 0.53 | 1.06 | 1.59 | 2.12 | 2.65 | 3.18 | 3.71 | 4.24 | 4.77 | 5.30 | 5.83 | 6.36 | 6.89 | 7.42 | 7.95 | 8.48 | 9.01 | 9.54 | 10.07 | 10.60 | 53% |

| 54% | 0.54 | 1.08 | 1.62 | 2.16 | 2.70 | 3.24 | 3.78 | 4.32 | 4.86 | 5.40 | 5.94 | 6.48 | 7.02 | 7.56 | 8.10 | 8.64 | 9.18 | 9.72 | 10.26 | 10.80 | 54% |

| 55% | 0.55 | 1.10 | 1.65 | 2.20 | 2.75 | 3.30 | 3.85 | 4.40 | 4.95 | 5.50 | 6.05 | 6.60 | 7.15 | 7.70 | 8.25 | 8.80 | 9.35 | 9.90 | 10.45 | 11.00 | 55% |

| 56% | 0.56 | 1.12 | 1.68 | 2.24 | 2.80 | 3.36 | 3.92 | 4.48 | 5.04 | 5.60 | 6.16 | 6.72 | 7.28 | 7.84 | 8.40 | 8.96 | 9.52 | 10.08 | 10.64 | 11.20 | 56% |

| 57% | 0.57 | 1.14 | 1.71 | 2.28 | 2.85 | 3.42 | 3.99 | 4.56 | 5.13 | 5.70 | 6.27 | 6.84 | 7.41 | 7.98 | 8.55 | 9.12 | 9.69 | 10.26 | 10.83 | 11.40 | 57% |

| 58% | 0.58 | 1.16 | 1.74 | 2.32 | 2.90 | 3.48 | 4.06 | 4.64 | 5.22 | 5.80 | 6.38 | 6.96 | 7.54 | 8.12 | 8.70 | 9.28 | 9.86 | 10.44 | 11.02 | 11.60 | 58% |

| 59% | 0.59 | 1.18 | 1.77 | 2.36 | 2.95 | 3.54 | 4.13 | 4.72 | 5.31 | 5.90 | 6.49 | 7.08 | 7.67 | 8.26 | 8.85 | 9.44 | 10.03 | 10.62 | 11.21 | 11.80 | 59% |

| 60% | 0.60 | 1.20 | 1.80 | 2.40 | 3.00 | 3.60 | 4.20 | 4.80 | 5.40 | 6.00 | 6.60 | 7.20 | 7.80 | 8.40 | 9.00 | 9.60 | 10.20 | 10.80 | 11.40 | 12.00 | 60% |

| 61% | 0.61 | 1.22 | 1.83 | 2.44 | 3.05 | 3.66 | 4.27 | 4.88 | 5.49 | 6.10 | 6.71 | 7.32 | 7.93 | 8.54 | 9.15 | 9.76 | 10.37 | 10.98 | 11.59 | 12.20 | 61% |

| 62% | 0.62 | 1.24 | 1.86 | 2.48 | 3.10 | 3.72 | 4.34 | 4.96 | 5.58 | 6.20 | 6.82 | 7.44 | 8.06 | 8.68 | 9.30 | 9.92 | 10.54 | 11.16 | 11.78 | 12.40 | 62% |

| 63% | 0.63 | 1.26 | 1.89 | 2.52 | 3.15 | 3.78 | 4.41 | 5.04 | 5.67 | 6.30 | 6.93 | 7.56 | 8.19 | 8.82 | 9.45 | 10.08 | 10.71 | 11.34 | 11.97 | 12.60 | 63% |

| 64% | 0.64 | 1.28 | 1.92 | 2.56 | 3.20 | 3.84 | 4.48 | 5.12 | 5.76 | 6.40 | 7.04 | 7.68 | 8.32 | 8.96 | 9.60 | 10.24 | 10.88 | 11.52 | 12.16 | 12.80 | 64% |

| 65% | 0.65 | 1.30 | 1.95 | 2.60 | 3.25 | 3.90 | 4.55 | 5.20 | 5.85 | 6.50 | 7.15 | 7.80 | 8.45 | 9.10 | 9.75 | 10.40 | 11.05 | 11.70 | 12.35 | 13.00 | 65% |

| 66% | 0.66 | 1.32 | 1.98 | 2.64 | 3.30 | 3.96 | 4.62 | 5.28 | 5.94 | 6.60 | 7.26 | 7.92 | 8.58 | 9.24 | 9.90 | 10.56 | 11.22 | 11.88 | 12.54 | 13.20 | 66% |

| 67% | 0.67 | 1.34 | 2.01 | 2.68 | 3.35 | 4.02 | 4.69 | 5.36 | 6.03 | 6.70 | 7.37 | 8.04 | 8.71 | 9.38 | 10.05 | 10.72 | 11.39 | 12.06 | 12.73 | 13.40 | 67% |

| 68% | 0.68 | 1.36 | 2.04 | 2.72 | 3.40 | 4.08 | 4.76 | 5.44 | 6.12 | 6.80 | 7.48 | 8.16 | 8.84 | 9.52 | 10.20 | 10.88 | 11.56 | 12.24 | 12.92 | 13.60 | 68% |

| 69% | 0.69 | 1.38 | 2.07 | 2.76 | 3.45 | 4.14 | 4.83 | 5.52 | 6.21 | 6.90 | 7.59 | 8.28 | 8.97 | 9.66 | 10.35 | 11.04 | 11.73 | 12.42 | 13.11 | 13.80 | 69% |

| 70% | 0.70 | 1.40 | 2.10 | 2.80 | 3.50 | 4.20 | 4.90 | 5.60 | 6.30 | 7.00 | 7.70 | 8.40 | 9.10 | 9.80 | 10.50 | 11.20 | 11.90 | 12.60 | 13.30 | 14.00 | 70% |

TAX FREE ADVANTAGE

Often, wealth advisors do not allocate to private investment strategies because of high tax exposure.

AAVUL eliminates this tax friction.

Eliminating tax friction increases client wealth.

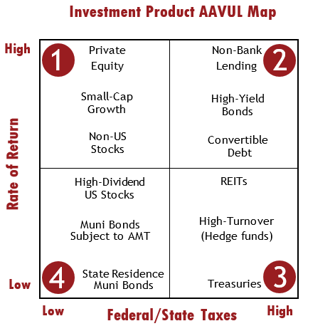

Tax aware investing usually only considers investment products exposed to income tax as candidates – corporate bonds; high yield bonds; non-US bonds; convertible securities; non-US dividends; REITs. Certainly, these products benefit by removing tax considerations from portfolio analysis. (See quadrants 2 and 3)

You may be surprised to learn that high performing products such as private equity or growth equity portfolios also gain substantial benefits. (See quadrant 1) This is true even though capital gains tax rates are lower than income tax rates (federal/state blended average of 29%) and gains are often realized sporadically.

Cross the Chasm

Receive a detailed portfolio and investment e-book defining the benefits of open architecture investing instead of using IDFs.

SAME FUND:

Use the Same Fund for AAVUL Investments

Before Advisable Wealth Engines, investment product firms wanting access to PPLI/PPVUL focused on insurance dedicated funds (IDFs). This is expensive and complex, and IDFs force the creation of a separate legal structure from the investment firm’s main products. And, this means a separate performance track record too.

Now, with AAVUL, an investment firm uses its existing fund (i.e. an LLC) to commingle AAVUL assets alongside institutional assets. IDFs are obsolete.

There are no additional cost or operational changes, and the existing fund’s performance history applies.

NEW CONVERSATIONS:

Bigger Planning Opportunities

Removing tax exposure from the investment decision encourages wealth advisors to allocate more to strategies with attractive return profiles; this freedom substantially changes an investment firm’s conversations when working with wealth advisors in the private wealth market.

While an investment firm’s products achieve enhanced returns inside AAVUL’s tax-free container, other products added alongside lead to a well-diversified, strategic portfolio in line with prudent investing standards. The investment program executing the client’s wealth plan achieves improved overall investment performance.

Note: An AAVUL open architecture portfolio requires a safe harbor allocation: no one investment can be more than 55% of the portfolio; no two more than 70%; no three more than 80%; no four more than 90%. This means an open architecture AAVUL portfolio achieves the safe harbor with a minimum of five investments. At this minimum and beyond, the AAVUL portfolio becomes a strategic, tax-free portfolio serving a private wealth client’s array of investments benefiting from AAVUL’s tax shield.