High Value in a Value Proposition

No other investment vehicle offers the array of client and advisor benefits than AAVUL.

EMBRACE IT:

Value Like No Other

“AAVUL’s tax saving profit means federal and state governments actually pay (i.e. more money in the pocket with the policy than without) each HNW, high-income policyowner to also have a death benefit worth millions of dollars. No other wealth planning or investment tool provides this benefit package.”

AAVUL for Tax Alpha

A one-step solution producing client profits plus advisor’s increased AUM.

Learn about AAVUL’s capabilities and its one-step tax management solution in our e-book.

HIGHLY EFFICIENT:

Growth & Death Benefit

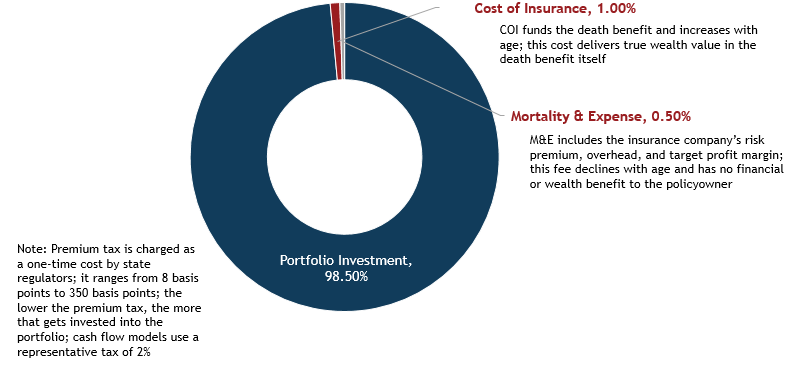

Aside from a state-imposed, one-time premium tax (ranging from 8 to 350 basis points), 99.5 cents of each dollar goes directly to your client’s benefit.

99.5 cents of each AAVUL dollar invested has a direct client benefit.

-

Investment Planning Impact: 98.5 cents (98.5%) is directly invested into the tax-free portfolio

-

Wealth Impact: 1 cent (1%) pays for the valuable death benefit

Only ½ of 1 cent (0.50%) goes to the insurance company for providing the AAVUL structure.

CALCULATE IT:

Projected Tax Savings to Portfolio Return

Q. What’s the blended federal and state tax rate and portfolio return combination needed to produce a desired AAVUL profit: policy tax savings > policy costs?

A. Use the Tax Shield Benefit (TSB) calculator

Inputs

Results

| This requires an integration of: | |

|---|---|

| Blended Federal/State Tax Rate | Rate of Return |

| 15% | 10.00% |

| 20% | 7.50% |

| 25% | 6.00% |

| 30% | 5.00% |

| 35% | 4.29% |

| 40% | 3.75% |

| 45% | 3.33% |

| 50% | 3.00% |

| 55% | 2.73% |

| 60% | 2.50% |

Interpretation A HNW client in the 35% blended tax bracket needs to achieve a AAVUL portfolio return of 4.29% to earn a tax profit of $0.00 for each dollar paid in policy expenses (at 1.5% policy costs to portfolio value).

Details

| Rate of Return | Gross Portofolio Value | Gross Profit | Total Taxes | After-Tax Profit | Total Policy Expenses | After-Policy-Expenses Profit | AAVUL Profit Net of Policy Expenses | Tax Shield Ratio(TSR) | Tax Savings to Total Taxes Paid | |

|---|---|---|---|---|---|---|---|---|---|---|

| 10.00% | $1,100,000 | $100,000 | $15,000 | $85,000 | $15,000 | $85,000 | $0.00 | 1.00 | $0.00 | |

| 7.50% | $1,075,000 | $75,000 | $15,000 | $60,000 | $15,000 | $60,000 | $0.00 | |||

| 6.00% | $1,060,000 | $60,000 | $15,000 | $45,000 | $15,000 | $45,000 | $0.00 | |||

| 5.00% | $1,050,000 | $50,000 | $15,000 | $35,000 | $15,000 | $35,000 | $0.00 | |||

| 4.29% | $1,042,857 | $42,857 | $15,000 | $27,857 | $15,000 | $27,857 | $0.00 | |||

| 3.75% | $1,037,500 | $37,500 | $15,000 | $22,500 | $15,000 | $22,500 | $0.00 | |||

| 3.33% | $1,033,333 | $33,333 | $15,000 | $18,333 | $15,000 | $18,333 | $0.00 | |||

| 3.00% | $1,030,000 | $30,000 | $15,000 | $15,000 | $15,000 | $15,000 | $0.00 | |||

| 2.73% | $1,027,273 | $27,273 | $15,000 | $12,273 | $15,000 | $12,273 | $0.00 | |||

| 2.50% | $1,025,000 | $25,000 | $15,000 | $10,000 | $15,000 | $10,000 | $0.00 |

Q. When does an AAVUL portfolio’s integration of policy costs, blended tax rate, and return turn from a tax shield loss to a profit?

A. Use the Tax Shield Ratio (TSR) calculator

Inputs

Results

| Blended Federal and State Tax Rate | Pre-Tax Rate of Return | Blended Federal and State Tax Rate | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1% | 2% | 3% | 4% | 5% | 6% | 7% | 8% | 9% | 10% | 11% | 12% | 13% | 14% | 15% | 16% | 17% | 18% | 19% | 20% | ||

| 15% | 0.15 | 0.30 | 0.45 | 0.60 | 0.75 | 0.90 | 1.05 | 1.20 | 1.35 | 1.50 | 1.65 | 1.80 | 1.95 | 2.10 | 2.25 | 2.40 | 2.55 | 2.70 | 2.85 | 3.00 | 15% |

| 16% | 0.16 | 0.32 | 0.48 | 0.64 | 0.80 | 0.96 | 1.12 | 1.28 | 1.44 | 1.60 | 1.76 | 1.92 | 2.08 | 2.24 | 2.40 | 2.56 | 2.72 | 2.88 | 3.04 | 3.20 | 16% |

| 17% | 0.17 | 0.34 | 0.51 | 0.68 | 0.85 | 1.02 | 1.19 | 1.36 | 1.53 | 1.70 | 1.87 | 2.04 | 2.21 | 2.38 | 2.55 | 2.72 | 2.89 | 3.06 | 3.23 | 3.40 | 17% |

| 18% | 0.18 | 0.36 | 0.54 | 0.72 | 0.90 | 1.08 | 1.26 | 1.44 | 1.62 | 1.80 | 1.98 | 2.16 | 2.34 | 2.52 | 2.70 | 2.88 | 3.06 | 3.24 | 3.42 | 3.60 | 18% |

| 19% | 0.19 | 0.38 | 0.57 | 0.76 | 0.95 | 1.14 | 1.33 | 1.52 | 1.71 | 1.90 | 2.09 | 2.28 | 2.47 | 2.66 | 2.85 | 3.04 | 3.23 | 3.42 | 3.61 | 3.80 | 19% |

| 20% | 0.20 | 0.40 | 0.60 | 0.80 | 1.00 | 1.20 | 1.40 | 1.60 | 1.80 | 2.00 | 2.20 | 2.40 | 2.60 | 2.80 | 3.00 | 3.20 | 3.40 | 3.60 | 3.80 | 4.00 | 20% |

| 21% | 0.21 | 0.42 | 0.63 | 0.84 | 1.05 | 1.26 | 1.47 | 1.68 | 1.89 | 2.10 | 2.31 | 2.52 | 2.73 | 2.94 | 3.15 | 3.36 | 3.57 | 3.78 | 3.99 | 4.20 | 21% |

| 22% | 0.22 | 0.44 | 0.66 | 0.88 | 1.10 | 1.32 | 1.54 | 1.76 | 1.98 | 2.20 | 2.42 | 2.64 | 2.86 | 3.08 | 3.30 | 3.52 | 3.74 | 3.96 | 4.18 | 4.40 | 22% |

| 23% | 0.23 | 0.46 | 0.69 | 0.92 | 1.15 | 1.38 | 1.61 | 1.84 | 2.07 | 2.30 | 2.53 | 2.76 | 2.99 | 3.22 | 3.45 | 3.68 | 3.91 | 4.14 | 4.37 | 4.60 | 23% |

| 24% | 0.24 | 0.48 | 0.72 | 0.96 | 1.20 | 1.44 | 1.68 | 1.92 | 2.16 | 2.40 | 2.64 | 2.88 | 3.12 | 3.36 | 3.60 | 3.84 | 4.08 | 4.32 | 4.56 | 4.80 | 24% |

| 25% | 0.25 | 0.50 | 0.75 | 1.00 | 1.25 | 1.50 | 1.75 | 2.00 | 2.25 | 2.50 | 2.75 | 3.00 | 3.25 | 3.50 | 3.75 | 4.00 | 4.25 | 4.50 | 4.75 | 5.00 | 25% |

| 26% | 0.26 | 0.52 | 0.78 | 1.04 | 1.30 | 1.56 | 1.82 | 2.08 | 2.34 | 2.60 | 2.86 | 3.12 | 3.38 | 3.64 | 3.90 | 4.16 | 4.42 | 4.68 | 4.94 | 5.20 | 26% |

| 27% | 0.27 | 0.54 | 0.81 | 1.08 | 1.35 | 1.62 | 1.89 | 2.16 | 2.43 | 2.70 | 2.97 | 3.24 | 3.51 | 3.78 | 4.05 | 4.32 | 4.59 | 4.86 | 5.13 | 5.40 | 27% |

| 28% | 0.28 | 0.56 | 0.84 | 1.12 | 1.40 | 1.68 | 1.96 | 2.24 | 2.52 | 2.80 | 3.08 | 3.36 | 3.64 | 3.92 | 4.20 | 4.48 | 4.76 | 5.04 | 5.32 | 5.60 | 28% |

| 29% | 0.29 | 0.58 | 0.87 | 1.16 | 1.45 | 1.74 | 2.03 | 2.32 | 2.61 | 2.90 | 3.19 | 3.48 | 3.77 | 4.06 | 4.35 | 4.64 | 4.93 | 5.22 | 5.51 | 5.80 | 29% |

| 30% | 0.30 | 0.60 | 0.90 | 1.20 | 1.50 | 1.80 | 2.10 | 2.40 | 2.70 | 3.00 | 3.30 | 3.60 | 3.90 | 4.20 | 4.50 | 4.80 | 5.10 | 5.40 | 5.70 | 6.00 | 30% |

| 31% | 0.31 | 0.62 | 0.93 | 1.24 | 1.55 | 1.86 | 2.17 | 2.48 | 2.79 | 3.10 | 3.41 | 3.72 | 4.03 | 4.34 | 4.65 | 4.96 | 5.27 | 5.58 | 5.89 | 6.20 | 31% |

| 32% | 0.32 | 0.64 | 0.96 | 1.28 | 1.60 | 1.92 | 2.24 | 2.56 | 2.88 | 3.20 | 3.52 | 3.84 | 4.16 | 4.48 | 4.80 | 5.12 | 5.44 | 5.76 | 6.08 | 6.40 | 32% |

| 33% | 0.33 | 0.66 | 0.99 | 1.32 | 1.65 | 1.98 | 2.31 | 2.64 | 2.97 | 3.30 | 3.63 | 3.96 | 4.29 | 4.62 | 4.95 | 5.28 | 5.61 | 5.94 | 6.27 | 6.60 | 33% |

| 34% | 0.34 | 0.68 | 1.02 | 1.36 | 1.70 | 2.04 | 2.38 | 2.72 | 3.06 | 3.40 | 3.74 | 4.08 | 4.42 | 4.76 | 5.10 | 5.44 | 5.78 | 6.12 | 6.46 | 6.80 | 34% |

| 35% | 0.35 | 0.70 | 1.05 | 1.40 | 1.75 | 2.10 | 2.45 | 2.80 | 3.15 | 3.50 | 3.85 | 4.20 | 4.55 | 4.90 | 5.25 | 5.60 | 5.95 | 6.30 | 6.65 | 7.00 | 35% |

| 36% | 0.36 | 0.72 | 1.08 | 1.44 | 1.80 | 2.16 | 2.52 | 2.88 | 3.24 | 3.60 | 3.96 | 4.32 | 4.68 | 5.04 | 5.40 | 5.76 | 6.12 | 6.48 | 6.84 | 7.20 | 36% |

| 37% | 0.37 | 0.74 | 1.11 | 1.48 | 1.85 | 2.22 | 2.59 | 2.96 | 3.33 | 3.70 | 4.07 | 4.44 | 4.81 | 5.18 | 5.55 | 5.92 | 6.29 | 6.66 | 7.03 | 7.40 | 37% |

| 38% | 0.38 | 0.76 | 1.14 | 1.52 | 1.90 | 2.28 | 2.66 | 3.04 | 3.42 | 3.80 | 4.18 | 4.56 | 4.94 | 5.32 | 5.70 | 6.08 | 6.46 | 6.84 | 7.22 | 7.60 | 38% |

| 39% | 0.39 | 0.78 | 1.17 | 1.56 | 1.95 | 2.34 | 2.73 | 3.12 | 3.51 | 3.90 | 4.29 | 4.68 | 5.07 | 5.46 | 5.85 | 6.24 | 6.63 | 7.02 | 7.41 | 7.80 | 39% |

| 40% | 0.40 | 0.80 | 1.20 | 1.60 | 2.00 | 2.40 | 2.80 | 3.20 | 3.60 | 4.00 | 4.40 | 4.80 | 5.20 | 5.60 | 6.00 | 6.40 | 6.80 | 7.20 | 7.60 | 8.00 | 40% |

| 41% | 0.41 | 0.82 | 1.23 | 1.64 | 2.05 | 2.46 | 2.87 | 3.28 | 3.69 | 4.10 | 4.51 | 4.92 | 5.33 | 5.74 | 6.15 | 6.56 | 6.97 | 7.38 | 7.79 | 8.20 | 41% |

| 42% | 0.42 | 0.84 | 1.26 | 1.68 | 2.10 | 2.52 | 2.94 | 3.36 | 3.78 | 4.20 | 4.62 | 5.04 | 5.46 | 5.88 | 6.30 | 6.72 | 7.14 | 7.56 | 7.98 | 8.40 | 42% |

| 43% | 0.43 | 0.86 | 1.29 | 1.72 | 2.15 | 2.58 | 3.01 | 3.44 | 3.87 | 4.30 | 4.73 | 5.16 | 5.59 | 6.02 | 6.45 | 6.88 | 7.31 | 7.74 | 8.17 | 8.60 | 43% |

| 44% | 0.44 | 0.88 | 1.32 | 1.76 | 2.20 | 2.64 | 3.08 | 3.52 | 3.96 | 4.40 | 4.84 | 5.28 | 5.72 | 6.16 | 6.60 | 7.04 | 7.48 | 7.92 | 8.36 | 8.80 | 44% |

| 45% | 0.45 | 0.90 | 1.35 | 1.80 | 2.25 | 2.70 | 3.15 | 3.60 | 4.05 | 4.50 | 4.95 | 5.40 | 5.85 | 6.30 | 6.75 | 7.20 | 7.65 | 8.10 | 8.55 | 9.00 | 45% |

| 46% | 0.46 | 0.92 | 1.38 | 1.84 | 2.30 | 2.76 | 3.22 | 3.68 | 4.14 | 4.60 | 5.06 | 5.52 | 5.98 | 6.44 | 6.90 | 7.36 | 7.82 | 8.28 | 8.74 | 9.20 | 46% |

| 47% | 0.47 | 0.94 | 1.41 | 1.88 | 2.35 | 2.82 | 3.29 | 3.76 | 4.23 | 4.70 | 5.17 | 5.64 | 6.11 | 6.58 | 7.05 | 7.52 | 7.99 | 8.46 | 8.93 | 9.40 | 47% |

| 48% | 0.48 | 0.96 | 1.44 | 1.92 | 2.40 | 2.88 | 3.36 | 3.84 | 4.32 | 4.80 | 5.28 | 5.76 | 6.24 | 6.72 | 7.20 | 7.68 | 8.16 | 8.64 | 9.12 | 9.60 | 48% |

| 49% | 0.49 | 0.98 | 1.47 | 1.96 | 2.45 | 2.94 | 3.43 | 3.92 | 4.41 | 4.90 | 5.39 | 5.88 | 6.37 | 6.86 | 7.35 | 7.84 | 8.33 | 8.82 | 9.31 | 9.80 | 49% |

| 50% | 0.50 | 1.00 | 1.50 | 2.00 | 2.50 | 3.00 | 3.50 | 4.00 | 4.50 | 5.00 | 5.50 | 6.00 | 6.50 | 7.00 | 7.50 | 8.00 | 8.50 | 9.00 | 9.50 | 10.00 | 50% |

| 51% | 0.51 | 1.02 | 1.53 | 2.04 | 2.55 | 3.06 | 3.57 | 4.08 | 4.59 | 5.10 | 5.61 | 6.12 | 6.63 | 7.14 | 7.65 | 8.16 | 8.67 | 9.18 | 9.69 | 10.20 | 51% |

| 52% | 0.52 | 1.04 | 1.56 | 2.08 | 2.60 | 3.12 | 3.64 | 4.16 | 4.68 | 5.20 | 5.72 | 6.24 | 6.76 | 7.28 | 7.80 | 8.32 | 8.84 | 9.36 | 9.88 | 10.40 | 52% |

| 53% | 0.53 | 1.06 | 1.59 | 2.12 | 2.65 | 3.18 | 3.71 | 4.24 | 4.77 | 5.30 | 5.83 | 6.36 | 6.89 | 7.42 | 7.95 | 8.48 | 9.01 | 9.54 | 10.07 | 10.60 | 53% |

| 54% | 0.54 | 1.08 | 1.62 | 2.16 | 2.70 | 3.24 | 3.78 | 4.32 | 4.86 | 5.40 | 5.94 | 6.48 | 7.02 | 7.56 | 8.10 | 8.64 | 9.18 | 9.72 | 10.26 | 10.80 | 54% |

| 55% | 0.55 | 1.10 | 1.65 | 2.20 | 2.75 | 3.30 | 3.85 | 4.40 | 4.95 | 5.50 | 6.05 | 6.60 | 7.15 | 7.70 | 8.25 | 8.80 | 9.35 | 9.90 | 10.45 | 11.00 | 55% |

| 56% | 0.56 | 1.12 | 1.68 | 2.24 | 2.80 | 3.36 | 3.92 | 4.48 | 5.04 | 5.60 | 6.16 | 6.72 | 7.28 | 7.84 | 8.40 | 8.96 | 9.52 | 10.08 | 10.64 | 11.20 | 56% |

| 57% | 0.57 | 1.14 | 1.71 | 2.28 | 2.85 | 3.42 | 3.99 | 4.56 | 5.13 | 5.70 | 6.27 | 6.84 | 7.41 | 7.98 | 8.55 | 9.12 | 9.69 | 10.26 | 10.83 | 11.40 | 57% |

| 58% | 0.58 | 1.16 | 1.74 | 2.32 | 2.90 | 3.48 | 4.06 | 4.64 | 5.22 | 5.80 | 6.38 | 6.96 | 7.54 | 8.12 | 8.70 | 9.28 | 9.86 | 10.44 | 11.02 | 11.60 | 58% |

| 59% | 0.59 | 1.18 | 1.77 | 2.36 | 2.95 | 3.54 | 4.13 | 4.72 | 5.31 | 5.90 | 6.49 | 7.08 | 7.67 | 8.26 | 8.85 | 9.44 | 10.03 | 10.62 | 11.21 | 11.80 | 59% |

| 60% | 0.60 | 1.20 | 1.80 | 2.40 | 3.00 | 3.60 | 4.20 | 4.80 | 5.40 | 6.00 | 6.60 | 7.20 | 7.80 | 8.40 | 9.00 | 9.60 | 10.20 | 10.80 | 11.40 | 12.00 | 60% |

| 61% | 0.61 | 1.22 | 1.83 | 2.44 | 3.05 | 3.66 | 4.27 | 4.88 | 5.49 | 6.10 | 6.71 | 7.32 | 7.93 | 8.54 | 9.15 | 9.76 | 10.37 | 10.98 | 11.59 | 12.20 | 61% |

| 62% | 0.62 | 1.24 | 1.86 | 2.48 | 3.10 | 3.72 | 4.34 | 4.96 | 5.58 | 6.20 | 6.82 | 7.44 | 8.06 | 8.68 | 9.30 | 9.92 | 10.54 | 11.16 | 11.78 | 12.40 | 62% |

| 63% | 0.63 | 1.26 | 1.89 | 2.52 | 3.15 | 3.78 | 4.41 | 5.04 | 5.67 | 6.30 | 6.93 | 7.56 | 8.19 | 8.82 | 9.45 | 10.08 | 10.71 | 11.34 | 11.97 | 12.60 | 63% |

| 64% | 0.64 | 1.28 | 1.92 | 2.56 | 3.20 | 3.84 | 4.48 | 5.12 | 5.76 | 6.40 | 7.04 | 7.68 | 8.32 | 8.96 | 9.60 | 10.24 | 10.88 | 11.52 | 12.16 | 12.80 | 64% |

| 65% | 0.65 | 1.30 | 1.95 | 2.60 | 3.25 | 3.90 | 4.55 | 5.20 | 5.85 | 6.50 | 7.15 | 7.80 | 8.45 | 9.10 | 9.75 | 10.40 | 11.05 | 11.70 | 12.35 | 13.00 | 65% |

| 66% | 0.66 | 1.32 | 1.98 | 2.64 | 3.30 | 3.96 | 4.62 | 5.28 | 5.94 | 6.60 | 7.26 | 7.92 | 8.58 | 9.24 | 9.90 | 10.56 | 11.22 | 11.88 | 12.54 | 13.20 | 66% |

| 67% | 0.67 | 1.34 | 2.01 | 2.68 | 3.35 | 4.02 | 4.69 | 5.36 | 6.03 | 6.70 | 7.37 | 8.04 | 8.71 | 9.38 | 10.05 | 10.72 | 11.39 | 12.06 | 12.73 | 13.40 | 67% |

| 68% | 0.68 | 1.36 | 2.04 | 2.72 | 3.40 | 4.08 | 4.76 | 5.44 | 6.12 | 6.80 | 7.48 | 8.16 | 8.84 | 9.52 | 10.20 | 10.88 | 11.56 | 12.24 | 12.92 | 13.60 | 68% |

| 69% | 0.69 | 1.38 | 2.07 | 2.76 | 3.45 | 4.14 | 4.83 | 5.52 | 6.21 | 6.90 | 7.59 | 8.28 | 8.97 | 9.66 | 10.35 | 11.04 | 11.73 | 12.42 | 13.11 | 13.80 | 69% |

| 70% | 0.70 | 1.40 | 2.10 | 2.80 | 3.50 | 4.20 | 4.90 | 5.60 | 6.30 | 7.00 | 7.70 | 8.40 | 9.10 | 9.80 | 10.50 | 11.20 | 11.90 | 12.60 | 13.30 | 14.00 | 70% |

Taxable Portfolio Cash Flow

Q. How does a taxable portfolio’s cash flows compare to a similar portfolio inside an AAVUL policy?

A. Use the AAVUL Cash Flow calculator.

Inputs

Results

| Gross Return of Tax Inefficient Investments | Taxable Portfolio Analysis | AAVUL Portfolio as the Asset Location Resource | AAVUL Portfolio Tax Alpha Benefit | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yr. | Age | Non-MEC, Multi-Pay Premium Schedule | Net of Invest-ment Fee Return | Taxable Portfolio Cash Value Gross Return | After-Tax Return | Tax Rate on Portfolio Income | Tax Amount | Taxable Portfolio Cash Value After Taxes | Premium Taxes | Insurance Charges | Cumulative Annual Policy Fees | AAVUL Portfolio Cash Value After Policy Fees | AAVUL Net Cash Value Advantage Over Taxable | Additional After-Tax Return to Taxable Cash Value | Death Benefit |

| 1 | 45 | $250,000 | 3.00% | $257,500 | 1.50% | 1.50% | $3,750 | $253,750 | $0 | $3,750 | $3,750 | $253,750 | $0 | 0.00% | |

| 2 | 46 | $250,000 | 3.00% | $522,725 | 1.50% | 1.50% | $7,556 | $511,306 | $0 | $7,556 | $7,556 | $511,306 | $0 | 0.00% | |

| 3 | 47 | $250,000 | 3.00% | $795,907 | 1.50% | 1.50% | $11,420 | $772,726 | $0 | $11,420 | $11,420 | $772,726 | $0 | 0.00% | |

| 4 | 48 | $250,000 | 3.00% | $1,077,284 | 1.50% | 1.50% | $15,341 | $1,038,067 | $0 | $15,341 | $15,341 | $1,038,067 | $0 | 0.00% | |

| 5 | 49 | $0 | 3.00% | $1,109,602 | 1.50% | 1.50% | $15,571 | $1,053,638 | $0 | $15,571 | $15,571 | $1,053,638 | $0 | 0.00% | |

| 6 | 50 | $0 | 3.00% | $1,142,891 | 1.50% | 1.50% | $15,805 | $1,069,442 | $0 | $15,805 | $15,805 | $1,069,442 | $0 | 0.00% | |

| 7 | 51 | $0 | 3.00% | $1,177,177 | 1.50% | 1.50% | $16,042 | $1,085,484 | $0 | $16,042 | $16,042 | $1,085,484 | $0 | 0.00% | |

| 8 | 52 | $0 | 3.00% | $1,212,493 | 1.50% | 1.50% | $16,282 | $1,101,766 | $0 | $16,282 | $16,282 | $1,101,766 | $0 | 0.00% | |

| 9 | 53 | $0 | 3.00% | $1,248,867 | 1.50% | 1.50% | $16,526 | $1,118,293 | $0 | $16,526 | $16,526 | $1,118,293 | $0 | 0.00% | |

| 10 | 54 | $0 | 3.00% | $1,286,333 | 1.50% | 1.50% | $16,774 | $1,135,067 | $0 | $16,774 | $16,774 | $1,135,067 | $0 | 0.00% | |

| 11 | 55 | $0 | 3.00% | $1,324,923 | 1.50% | 1.50% | $17,026 | $1,152,093 | $0 | $17,026 | $17,026 | $1,152,093 | $0 | 0.00% | Death Benefit Determined Using Age and Health Underwriting Factors |

| 12 | 56 | $0 | 3.00% | $1,364,671 | 1.50% | 1.50% | $17,281 | $1,169,374 | $0 | $17,281 | $17,281 | $1,169,374 | $0 | 0.00% | |

| 13 | 57 | $0 | 3.00% | $1,405,611 | 1.50% | 1.50% | $17,541 | $1,186,915 | $0 | $17,541 | $17,541 | $1,186,915 | $0 | 0.00% | |

| 14 | 58 | $0 | 3.00% | $1,447,780 | 1.50% | 1.50% | $17,804 | $1,204,719 | $0 | $17,804 | $17,804 | $1,204,719 | $0 | 0.00% | |

| 15 | 59 | $0 | 3.00% | $1,491,213 | 1.50% | 1.50% | $18,071 | $1,222,790 | $0 | $18,071 | $18,071 | $1,222,790 | $0 | 0.00% | |

| 16 | 60 | $0 | 3.00% | $1,535,949 | 1.50% | 1.50% | $18,342 | $1,241,131 | $0 | $18,342 | $18,342 | $1,241,131 | $0 | 0.00% | |

| 17 | 61 | $0 | 3.00% | $1,582,028 | 1.50% | 1.50% | $18,617 | $1,259,748 | $0 | $18,617 | $18,617 | $1,259,748 | $0 | 0.00% | |

| 18 | 62 | $0 | 3.00% | $1,629,489 | 1.50% | 1.50% | $18,896 | $1,278,645 | $0 | $18,896 | $18,896 | $1,278,645 | $0 | 0.00% | |

| 19 | 63 | $0 | 3.00% | $1,678,373 | 1.50% | 1.50% | $19,180 | $1,297,824 | $0 | $19,180 | $19,180 | $1,297,824 | $0 | 0.00% | |

| 20 | 64 | $0 | 3.00% | $1,728,724 | 1.50% | 1.50% | $19,467 | $1,317,292 | $0 | $19,467 | $19,467 | $1,317,292 | $0 | 0.00% | |

| 21 | 65 | $0 | 3.00% | $1,780,586 | 1.50% | 1.50% | $19,759 | $1,337,051 | $0 | $19,759 | $19,759 | $1,337,051 | $0 | 0.00% | |

| 22 | 66 | $0 | 3.00% | $1,834,004 | 1.50% | 1.50% | $20,056 | $1,357,107 | $0 | $20,056 | $20,056 | $1,357,107 | $0 | 0.00% | |

| 23 | 67 | $0 | 3.00% | $1,889,024 | 1.50% | 1.50% | $20,357 | $1,377,463 | $0 | $20,357 | $20,357 | $1,377,463 | $0 | 0.00% | |

| 24 | 68 | $0 | 3.00% | $1,945,695 | 1.50% | 1.50% | $20,662 | $1,398,125 | $0 | $20,662 | $20,662 | $1,398,125 | $0 | 0.00% | |

| 25 | 69 | $0 | 3.00% | $2,004,065 | 1.50% | 1.50% | $20,972 | $1,419,097 | $0 | $20,972 | $20,972 | $1,419,097 | $0 | 0.00% | |

| 26 | 70 | $0 | 3.00% | $2,064,187 | 1.50% | 1.50% | $21,286 | $1,440,384 | $0 | $21,286 | $21,286 | $1,440,384 | $0 | 0.00% | |

| 27 | 71 | $0 | 3.00% | $2,126,113 | 1.50% | 1.50% | $21,606 | $1,461,989 | $0 | $21,606 | $21,606 | $1,461,989 | $0 | 0.00% | |

| 28 | 72 | $0 | 3.00% | $2,189,896 | 1.50% | 1.50% | $21,930 | $1,483,919 | $0 | $21,930 | $21,930 | $1,483,919 | $0 | 0.00% | |

| 29 | 73 | $0 | 3.00% | $2,255,593 | 1.50% | 1.50% | $22,259 | $1,506,178 | $0 | $22,259 | $22,259 | $1,506,178 | $0 | 0.00% | |

| 30 | 74 | $0 | 3.00% | $2,323,261 | 1.50% | 1.50% | $22,593 | $1,528,771 | $0 | $22,593 | $22,593 | $1,528,771 | $0 | 0.00% | |

| 31 | 75 | $0 | 3.00% | $2,392,959 | 1.50% | 1.50% | $22,932 | $1,551,702 | $0 | $22,932 | $22,932 | $1,551,702 | $0 | 0.00% | |

| 32 | 76 | $0 | 3.00% | $2,464,748 | 1.50% | 1.50% | $23,276 | $1,574,978 | $0 | $23,276 | $23,276 | $1,574,978 | $0 | 0.00% | |

| 33 | 77 | $0 | 3.00% | $2,538,690 | 1.50% | 1.50% | $23,625 | $1,598,603 | $0 | $23,625 | $23,625 | $1,598,603 | $0 | 0.00% | |

| 34 | 78 | $0 | 3.00% | $2,614,851 | 1.50% | 1.50% | $23,979 | $1,622,582 | $0 | $23,979 | $23,979 | $1,622,582 | $0 | 0.00% | |

| 35 | 79 | $0 | 3.00% | $2,693,296 | 1.50% | 1.50% | $24,339 | $1,646,920 | $0 | $24,339 | $24,339 | $1,646,920 | $0 | 0.00% | |

| 36 | 80 | $0 | 3.00% | $2,774,095 | 1.50% | 1.50% | $24,704 | $1,671,624 | $0 | $24,704 | $24,704 | $1,671,624 | $0 | 0.00% | |

| 37 | 81 | $0 | 3.00% | $2,857,318 | 1.50% | 1.50% | $25,074 | $1,696,698 | $0 | $25,074 | $25,074 | $1,696,698 | $0 | 0.00% | |

| 38 | 82 | $0 | 3.00% | $2,943,038 | 1.50% | 1.50% | $25,450 | $1,722,149 | $0 | $25,450 | $25,450 | $1,722,149 | $0 | 0.00% | |

| 39 | 83 | $0 | 3.00% | $3,031,329 | 1.50% | 1.50% | $25,832 | $1,747,981 | $0 | $25,832 | $25,832 | $1,747,981 | $0 | 0.00% | |

| 40 | 84 | $0 | 3.00% | $3,122,269 | 1.50% | 1.50% | $26,220 | $1,774,201 | $0 | $26,220 | $26,220 | $1,774,201 | $0 | 0.00% | |

KNOW IT:

Peerless Benefit Package; What’s Not to Like?

![]()

Advisor Led

You are the builder, manager, and monitor of the AAVUL portfolio and keep the AUM

![]()

Inflation Protection

The death benefit’s purchasing power is inflation protected since the benefit amount is a function of the AAVUL portfolio’s value

![]()

Open Architecture

Use any of your advisory firm’s preferred investments

![]()

Compounding Client ROI

Your high-income, HNW clients using AAVUL can expect profits (i.e. tax savings > policy expenses) that accelerate over time from compounding of the net tax savings

![]()

Valuable Death Benefit

The tax-free death benefit adds a highly valuable planning tool for asset protection, wealth transfers, wealth replacement, and charitable giving

![]()

Portfolio Integration

The portfolio is an integrated, tax-free portfolio companion to each HNW client’s other investment portfolios, and it remains under your wealth planning oversight

DO IT:

Key Planning Recommendation

Tax-deferred portfolios such as IRAs, annuities, and deferred compensation only offer tax alpha benefits if the income tax rate in retirement is lower than during the working years; what is called the tax-bracket arbitrage.

For HNW, high-income clients in which retirement income tax rates will remain high, AAVUL is a superior investment solution.

PLANNING TACTIC

Counter to common convention, it’s a much better strategy for clients with substantial cash flow during the working years to pay taxes in the current tax year and secure increased future wealth.

TIPS

1) Execute a one-time conversion from traditional IRAs to Roth (what is known as a back-door conversion)

2) Invest additional annual post-tax wealth aggressively into AAVUL (no contribution limits)

RESULTS

-

Gain full tax-free treatment for the portfolio

-

Eliminate required distributions (and higher retirement tax bills)

-

Provide flexible, tax-free retirement income to support a variety of wealth planning needs (if needed)

-

Uncomplicate beneficiary designations

-

Use AAVUL’s death benefit for wealth transfers, wealth replacement, and charitable giving