Blog

Our blogs focus on AAVUL's many wealth and investment planning applications.

Client Profitability; In the Client’s Best Interest

“Invest for maximum total REAL return. This means the return on invested dollars after taxes and after inflation. This is the only rational objective for most long-term investors. Any investment strategy that fails to recognize the insidious effect of taxes and inflation fails to recognize the true nature of the investment environment and thus is severely handicapped.” John Templeton

“Invest for maximum total REAL return. This means the return on invested dollars after taxes and after inflation. This is the only rational objective for most long-term investors. Any investment strategy that fails to recognize the insidious effect of taxes and inflation fails to recognize the true nature of the investment environment and thus is severely handicapped.” John Templeton

Embedded in the Fiduciary Rule discussion is the advisor’s compensation, with the rule’s explicit preference for fee-based versus commission-based services. While there are substantial debates about the merits of either approach, the client’s costs for financial and investment advice are the central focus.

The CFA 2016 study, “From Trust to Loyalty: What Investors Want”, found the two top reasons (of 14 in total) a client would fire an advisor are underperformance (53%) and fee increases (46%). And, of 11 top-tier attributes an advisor must have, three were fee related:

#1: “Fully discloses fees and other costs” (80%)

#3: “Clearly explains all fees and costs before they are charged” (79%)

#9: “Charges fees that reflect the value I get from the relationship” (71%)

Of course, if there weren’t benefits associated with the costs no one would hire an advisor (i.e. the #9 reason), but the practice management challenge advisors face is developing a formula for showing clients the dollar-based benefits to contrast with the out-of-pocket costs. Like it or not, many clients have some measure of a nagging anxiety wondering if the costs they pay are “a good deal” compared to what another advisor could offer or, even, going it alone.

Calculating an Advisor’s Value

Vanguard and Russell Investments have both measured an advisor’s added value; Vanguard calculates the benefit at 3% and Russell at 3.75%

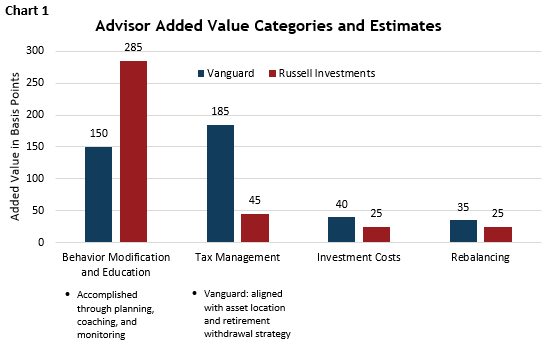

Naturally, an advisor’s biggest impact is modifying the client’s spending and investing behavior. This is accomplished through planning services and an advisor-client accountability relationship.

However, among an advisor’s non-planning, tactical services, tax management has the highest impact, substantially beating portfolio rebalancing and investment fees as shown in Chart 1.

Advisor Added Value Categories and Estimates

The advisor’s added value translates to more wealth through the advisor’s actions than had the investor operated independently.

The Client Profitability Equation

Stepping away from accounting-like profit definitions, the client formula is quite simple:

Cash Inflows from the advisor’s services (“Benefits”) > Cash Outflows for the advisor’s fees (“Costs”) = Profits

The profit notion here is actually spoken as: “Did I have more money from my advisor’s actions net of the fees I paid?”

Building from the CFA study’s conclusions, there are two interrelated ways an advisor produces client profits:

- Better Investment Results: The Fiduciary’s Open Architecture Advantage

Compared to a commission-based advisor, a fiduciary advisor has a built-in advantage in calculating Benefits from the executed investment plan. Essentially, a fiduciary seeks investment efficiency first (known as “Beta”) and investment bets second (“Alpha”). Transaction-based compensation motives are not considered.

In other words, making investment decisions for the client’s best interest (i.e. the heart of the fiduciary rule debate) allows an advisor to freely integrate lower investment costs in which ETFs and/or passive mutual funds serve as the portfolio’s core instead of more expensive (and possibly proprietary) active options.

With the core driving the primary investment structure for the short- and mid-term planning horizons, the fiduciary advisor can make supplemental allocations to long-term portfolio satellite positions; common satellites being aggressive fixed income (e.g. high yield; convertible bonds; non-US), non-US stocks, small cap growth, REITs, and alternative investments (e.g. hedge funds; direct lending; private equity).

Therefore, an advisor with a true open architecture investment palette in a core (beta)/satellite (alpha) structure has a distinct and repeatable advantage in showing how blended investments produce higher fee efficiency than a single strategy approach such as passive only or active only. (Fee efficiency being the return received for the fee-dollars paid.)

- Fewer Leakages: Minimizing Losses Allows Compounding from a Higher Floor

In addition to high investment costs, there are three other key ways that wealth is lost: market downturns; overspending; taxes. These leakages have been covered in the blog “Preserving Wealth through Tax Alpha”. Each dollar that is NOT lost allows the portfolio to compound from a higher floor; this has real economic importance for a client’s wealth creation.

While client behavior modification has the highest advisor impact (from the above Vanguard and Russell studies), it’s also the most difficult to quantify. The four leakage categories, in contrast, can be calculated by comparing the executed plan to other options.

- Portfolio stability during periods of downside market volatility (i.e. using the max drawdown statistic to compare the executed portfolio to one not using risk management)

- Spending (and savings) before and after the wealth plan

- A portfolio mixing passive and active to one with all actively managed investment products (see #1 above)

- Tax savings from a tax management program (Tax Alpha) to a portfolio that doesn’t consider tax implications (see below)

Advisor-Applied VUL (AAVUL) Bringing Enhanced Client Profitability

AAVUL provides perfect tax efficiency (a tax shield) in a single step. And, AAVUL products come with no sales commissions, trailers, or surrender charges, in addition to having low internal costs.

For a given dollar, 98% to 99% of the invested amount in AAVUL goes into the tax-free portfolio, with the majority of the policy’s costs applied to a valuable death benefit.

AAVUL’s tax shield is the interplay between three factors: 1) the client’s blended federal/state income and capital gains tax rates, 2) the AAVUL’s portfolio return, and 3) the policy’s costs.

AAVUL’s client profitability equation is: Tax Savings – Policy Costs = Profits

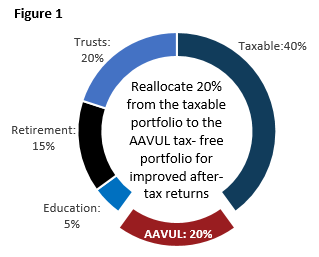

As Figure 1 shows for a typical HNW portfolio, simply taking investments that benefit most from AAVUL’s tax shield (corporate bonds, high yield bonds; convertible bonds; tactical allocation models; non-US stocks and bonds; REITs; direct lending; hedge funds; small cap growth; private equity) from the HNW client’s taxable portfolio and asset locating them inside an AAVUL policy generates compounding client profits over time (see the blog “Asset Location: Meaningful, Clear, and Easy”).

The client’s profitability has a remarkable outcome: AAVUL’s tax savings (provided by federal and state laws and regulations less the policy’s expenses) essentially gives the client increasing wealth at a compounding rate while also providing a tax-free death benefit worth millions of dollars. This death benefit then leads the advisor to a valuable implementation tool for wealth transfers, wealth replacement, and charitable giving.

Truly, no other wealth planning tool offers such a wealth-creation package.

The Fiduciary’s Obligation

Many advisors possess biases against insurance products from bad experiences with complexity and high or hidden costs, combined with difficult distribution relationships. Few would dispute the caution that evolves.

Nonetheless, innovation has been occurring in the insurance industry. The fiduciary advisor’s determination to use the best planning and investment solutions must consider this innovation in the full package that AAVUL offers HNW clients.

- One-step tax alpha that provides client profitability at an increasing rate (i.e. reinvesting the tax savings net of the policy’s expenses)

- Tax-free cash access providing an important funding resource for a variety of wealth-planning applications

- While receiving the tax shield’s increased wealth, gaining a valuable and tax-free death benefit

- Applying the death benefit to a client’s wealth transfer, wealth replacement, and charitable giving goals

An advisor that produces ongoing summaries proving the profitable outcomes he or she produces for each client solidifies the client’s trust.

Whereas many profit-making advisory tactics occur sporadically, tax management generates benefits continually. Using AAVUL takes these benefits to an even higher level with tax-free results (vs. tax deferred) and an associated death benefit that directly adds to the family’s long-term wealth.

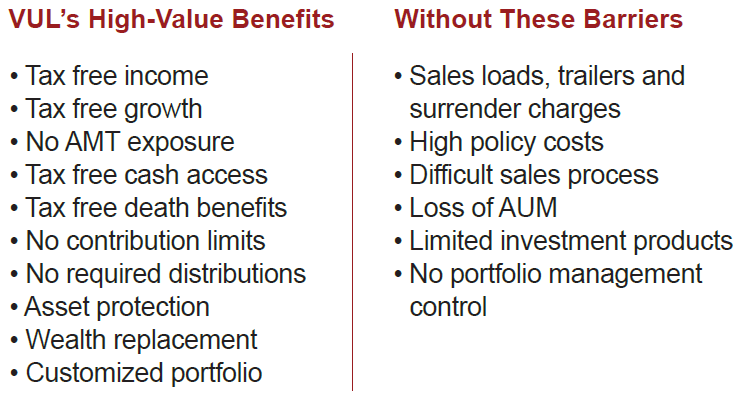

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

The new Advisor-Applied VUL.

It’s low-cost, one-step tax alpha.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.