IDFs are Obsolete; Go Open Architecture

Open architecture AAVUL portfolios outperform while keeping you, the advisor, in charge.

IDFs Fail the AAVUL Mandate;

Open Architecture Prevails

An AAVUL policy is the most profoundly capable wealth planning tool available to you for your HNW, high-income clients (the clients that drive your advisory firm’s profitability; the clients every competitor wants to steal).

Insurance Dedicated Funds (IDFs) often fail in providing portfolio returns to take advantage of AAVUL’s many benefits, especially its tax-free structure.

When you’re in charge, an open architecture portfolio (using your preferred investments and portfolio structure) is far more likely than IDFs to generate compounding profits within the policy (lasting decades).

Cross the Chasm

A detailed IDF review with numerous “first-of-its-kind” analysis.

Learn about AAVUL portfolio and investing, including a client game plan in our e-book.

Piercing the Tax Shield

There are two ways to pierce AAVUL’s tax shield:

1) Failure to satisfy a legally mandated minimum diversification formula, and/or

2) The policy-owner gives evidence that he or she controls the investment decisions in the portfolio (i.e. “the investor control doctrine”).

Executing Weber's Boundaries Through Technology

Learn about AAVUL’s legal and regulatory foundation and how investing and compliance technology transforms both the AAVUL portfolio (open architecture) and your role (the portfolio's builder, manager, and monitor).

Download the e-book and its associated infographic or visit our Legal View page for more information.

IDFs Defined:

An insurance dedicated fund (IDF) is a special purpose investment vehicle just for insurance variable contracts (annuities and variable universal life).

An IDF investment strategy is a clone of another non-insurance vehicle (i.e. the “mother strategy”), predominately hedge funds.

However, each IDF must have its own seed capital, legal structure, tax filings, audit, operations, fees, custody, and, especially important to attract new investors, its own investment track record.

IDFs Don’t Solve for Investor Control

IDFs – or other, similar options such as LLCs or single manager insurance company separate accounts – don’t do anything by themselves to solve for investor control exposure.

The tax shield can be pierced (and tax benefits lost plus possible penalties).

Investor control is not a structural issue, but one focused solely on the policyowner’s unique “facts and circumstances”.

IDFs Are Not a Fiduciary Portfolio

A single IDF is not a portfolio according to the fiduciary definition.

An IDF structure violates a number of longstanding portfolio construction principles, the principles used by fiduciary advisors like you when building, managing, and monitoring client portfolios.

-

Concentration Risk

-

Asset Class Structural Risk

-

Style Risk

-

Manager Risk

-

High Investment Costs

-

Limited Investment Histories

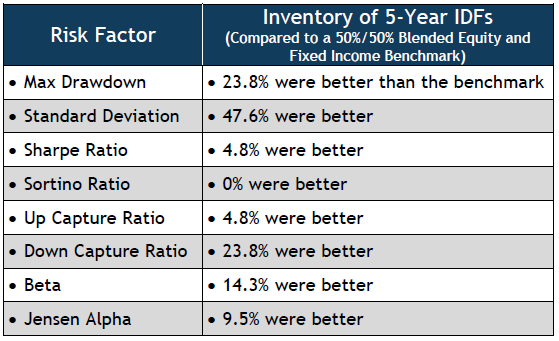

These fiduciary violations reveal themselves in the universe of IDFs delivering substandard risk control measures compared to a blended 50%/50% fixed income to equity benchmark.

Source: Advisable Wealth Engines

Don’t Know? Don’t Offer

You won’t offer investments to your clients that you don’t understand.

(Source: 2016 Jefferson National “Annual Advisor Authority”)

With so many fiduciary compromises when using IDFs, few advisors are willing to accept the liability exposure that results, even with AAVUL’s many benefits.

Open Architecture for the Fiduciary Advisor

Open architecture, optimized AAVUL portfolios are a no-compromises, straight-line application of your fiduciary mandate.

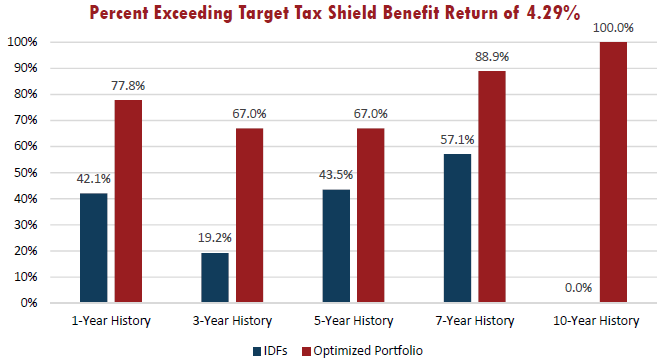

To compare IDFs to open architecture/optimized portfolios, this scenario is used:

1) A HNW, high-income client in the 35% federal/state blended

tax bracket

2) AAVUL policy expenses averaging 1.5%

CHALLENGE

What percent of the two portfolio structures – IDFs vs. Open Architecture/Optimized – achieve at least a 4.29% portfolio return?

This is the return that produces at least a breakeven tax shield benefit ($1 of policy expenses = $1 of tax shield savings).

Note: a return greater than 4.29% leads to a policyowner profit (i.e. tax savings > policy expenses); less than 4.29% results in a policyowner loss (i.e. policy expenses > tax savings)

IT’S NO CONTEST

Fiduciary-based portfolios roundly outperform IDFs (which are concentrated and unoptimized investments).

Source: Advisable Wealth Engines