Blog

Our blogs focus on AAVUL's many wealth and investment planning applications.

Controlling Expectations and Outcomes

The present economic climate offers heightened insecurity that recalls the traumatic memories from 2008. As far as investing is concerned, clients look to their advisers for precise navigation through these churning waters with the expectation/hope that “the outcomes from this next cycle will be different.”

Defining an Outcome

An outcome is different than a goal. The latter represents a forward view—what we want to happen; whereas an outcome is the result of the planning—what did happen.

Think of the distinction this way. A client goal might be, “I want my wealth secured for the long term,” and the related outcome is, “Your portfolio avoided losses.” While outcomes occur with or without planning, a well-executed plan sets the course for more positive outcomes.

Expectations and Outcomes

The adviser is the primary source for executing the plan, but only one of several sources for setting expectations (see a September 2014 Practice Management Blog post titled “Neutralizing a Client’s Negative External Influences”). A client that expects a 10 percent return because “that’s what my friend’s adviser delivered” only to be disappointed when 8 percent is realized brings to light a failure in managing expectations not execution.

Nonetheless, unmet expectations damage relationships. Therefore, communication strategies form the foundation for setting expectations and defining reasonable outcomes, and this process begins with the plan’s formulation through to each quarterly meeting; it never stops. (Note: fulfilling a client’s service and communication expectations are wholly under an adviser’s control. Take advantage of this control and nail it!)

Any Dollar Lost has the Same Outcome

The current bull market is the third longest in history. The natural cycle means there’s a much higher probability of a market decline than a continued increase. If expectations for the plan’s execution solely rest on performance numbers that go up, there’s a business risk associated with a dissatisfied client base.

Let me state the obvious: a performance decline means the dollar value of the portfolio is reduced; dollars are lost from wealth. This is a simple but vital message to reinforce. Why? Because any dollar lost from wealth—from spending, taxes, fees, depreciation or uninsured risks—has the same effect as a dollar lost to the market.

Here’s the dilemma: so much client anxiety is focused on market downturns that are largely out of an adviser’s control. And, the adviser, knowing this anxiety exists, gets stressed over the possibility that his or her top clients may start looking for another practitioner should investment performances stumble.

Seizing Control of Outcomes

Pounding the fact that any dollar lost has the same wealth outcome as a market decline shifts the plan’s tactical target to programs that minimize the loss of dollars. Given this blog’s space limitation, we’ll focus on two tactics: one for an adviser’s top clients and one for all clients.

Top Clients: Tax Management

The current tax environment is unfavorable to high-income investors. In some states, the combined tax burden can exceed 50 percent, but even the federal 40 percent marginal tax rate takes substantial dollars from wealth every year. In other words, investors worried about a big market decline every five or six years (U.S Trust says 65 percent of wealthy investors’ priority is to minimize taxes), miss the point that an effective tax management program can minimize the loss of dollars every year. This is called tax alpha and it can be a primary (and controlled) source of outcomes produced by an adviser. Consider variable universal life, variable annuities and trusts in an effective tax management solution.

All Clients: Products with a Disciplined Selling System

Many studies chronicle the difficulty in actively managed investment products exceeding benchmarks. Whereas most managers tout their stock research and “buying” systems, certain portfolio managers have highly disciplined “selling” systems that do two things to capture value: 1) selling on the upside when a target value is hit; and 2) selling on the downside when value floors are reached.

Losing less than the market also produces excess return. Investment products excelling in the risk statistics “downside capture” and “downside deviation” accurately identify portfolio managers with disciplined selling systems. Here’s the impact: studies show that avoiding losses leads to a better long-term performance profile simply because each dollar NOT lost allows the portfolio to compound from a higher floor.

Comparing Outcomes

In the annual—if not quarterly—review meeting, produce a side-by-side comparison of the plan’s loss minimization program and one without. This will illustrate how the outcome of extra dollars measurably defines a client’s ROI in the advisory relationship.

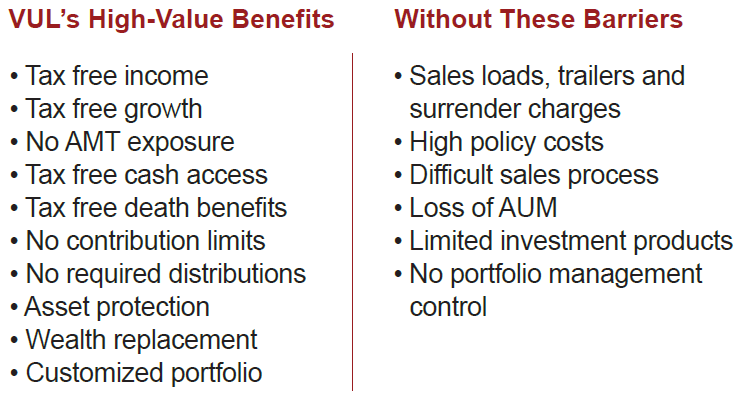

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.