Blog

Our blogs focus on AAVUL's many wealth and investment planning applications.

Better Performance: Higher After-Tax Returns through Tax Alpha

It’s amazing how one day can change a client’s thinking about portfolio performance. Leading up to December 31st, communication and reporting form expectations, but on January 1st, these expectations transform to a client’s reality.

“Did my portfolio meet its target?”

“Is my plan on track?”

Money Produced More Efficiently

Since performance is numerically driven, it’s easy for clients to focus on the report itself and lose sight of how an investment program executes a wealth plan. Beneath the tables and charts is a core element essential for funding a wealth plan: investment efficiency.

“You can’t create wealth unless you first protect it.”

Efficiency considers the portfolio amount at the beginning of the year and the amount left over after accounting for increases (deposits, portfolio income and growth) and leakages (market losses, if any, fees, taxes and withdrawals). These leakages, regardless of the source, cause dollars to be lost. And, not just a single dollar, but the compounded value of a lost dollar. Leakages result in inefficiency, leading to an important truism – you can’t create wealth unless you first protect it.

Therefore, each year a primary objective is to maximize the portfolio’s net dollar amount, or, spoken through the client’s view, “Having more money in my pocket.”

Funding through Dollars not Percentages

This dollar-level view is critical in understanding the investment program’s track to funding the client’s needs and aspirations. In other words, needs aren’t funded through percentages and investment statistics, but through dollars. An investment plan that isn’t producing sufficient dollars in the short-, mid-, and long-term horizons will fail the client regardless of whether portfolio performance exceeds a benchmark.

“Income needs aren’t funded through percentages.

They’re funded through dollars.”

Adding Value through Control

An advisor can’t control market performance. The two areas that enable an advisor to affect directly the production of net investment dollars are: 1) investment fees and 2) tax alpha.

“Higher investment fees are a drag on performance.”

Advisors continue gravitating to low-cost ETFs and mutual funds. Higher product fees that don’t produce better returns cause inefficiency, and this results in a drag on investment performance. However, fee efficiency impacts performance at the margins and not at the portfolio’s core. (Fee efficiency being the amount of return per dollar of fees paid.)

Much more significant to portfolio performance is the erosive impact of portfolio income and capital gains taxes.

“Tax leakage every year quickly erodes wealth.”

Investment return is comprised of two sources: income (interest or dividends) and appreciation (above cost basis). Both these sources are exposed to taxes. Whereas the difference between low- and high-cost investment product fees may be 1% to 2%, portfolio taxes cut deeply into return, over 50% in marginal rates in high-tax states.

This significant tax leakage occurring each year quickly erodes wealth; these tax payments are lost to compounding. For this reason, tax-free portfolios, such as institutions enjoy, have a much smoother growth trajectory simply from compounding the tax savings.

“Control what you can; tax alpha.”

Tax Alpha for Added Value

The concept of “added value” is simple: “Was more value produced than the costs?” For many advisory services, it’s difficult to point directly to specific actions that add value to clients’ wealth. Tax alpha is one service that an advisor controls, and one that delivers a path to accelerated wealth creation.

The key is to generate this added value for the client at the lowest possible cost, just like the difference between active and passive investing. Tax alpha through advisor applied variable universal life (AAVUL) insurance is a tax-free portfolio that produces tax alpha in one step compared to other tax alpha tactics that are laborious (e.g. tax-loss harvesting; income shifting; product selection). Clients with blended federal and state tax rates of 35% or higher will reach breakeven from AAVUL (net of expenses) in a few years or less, with compounded wealth creation lasting decades.

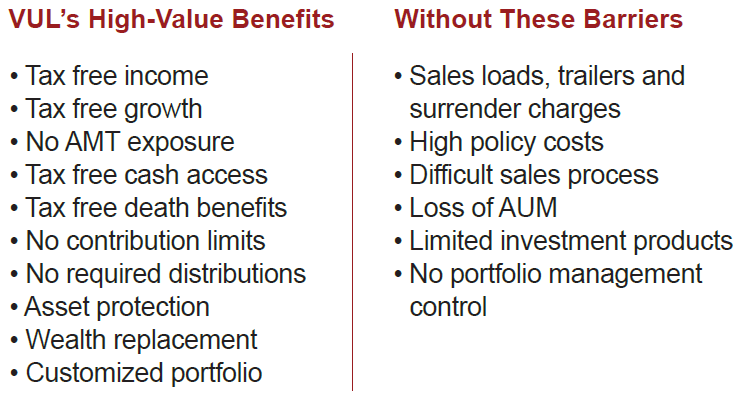

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

The new Advisor-Applied VUL.

It’s low-cost, one-step tax alpha.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.