Blog

Our blogs focus on AAVUL's many wealth and investment planning applications.

A Client Base for High Valuation

Wealth management professionals face a key business constraint in the limited number of advice-giving hours in a day. Since revenues are ultimately tied to the value of each advice hour, at capacity, an adviser’s growth options are limited.

The competitive market eliminates the option of raising fees. Another alternative is to increase the productivity of each hour with two oft-cited tactics: 1) gaining productivity through technology; and 2) replacing low-AUM clients with high-AUM clients. Certainly, expanding to the emerging affluent segment would be counterproductive to a one-to-one client service model, but what if a scaled service model were used?

Culling Based on AUM Fails a Growth Strategy

An advice hour spent with a high-AUM client will produce more revenue than one with a low-AUM client. In a one-to-one relationship model, culling low-AUM clients improves efficiency per hour, but there are three critical pitfalls to this approach for an advisory firm interested in a larger market footprint and a higher firm valuation.

- It’s hard to win high-AUM clients. The higher a prospective client’s AUM, the more intense the competition and there can be only one winner. When an adviser loses to the competition, those hours spent in marketing represent an opportunity cost.

- Withdrawals and wealth transfers. The largest segment of the high-AUM market is made up of people in or near retirement. As the years pass, a high net worth client’s AUM will be flat or declining through withdrawals and/or wealth transfers.

- A firm’s valuation has a forward view of AUM. P&L performance is an important input to a firm’s valuation, but this only shows current-year metrics. Most important to an acquirer is the future AUM profile. A client base made up of high-AUM retiree clients will be much less attractive than a client base with a significant portion of clients in their wealth-accumulation phase.

The Emerging Affluent Segment’s Appeal

The emerging affluent client (AUM between $100,000 and $250,000 and under 45 years of age) will grow to high-value AUM over time through career advancements and wealth transfers. Since there are tens of millions more in this segment today than those with AUM greater than $1,000,000, there’s a large prospect pool in every local market. These are important factors in valuing future AUM.

The tactical issue is developing an advice and investment package, combined with volume service techniques, allowing an adviser’s advice-giving hours to be efficiently utilized. Should an adviser institute such a solution (and in parallel with the adviser’s high-AUM client base), future AUM grows exponentially as does the firm’s valuation.

Keeping Advice as the Key Differentiator

The emerging affluent have common planning needs such as budgeting, education, retirement, tax management, and portfolio design. Indeed, the concepts within each planning category hold tight individual to individual, with the differences only on the demographic margins—like the number of children, income, budget priorities, etc.

People with common needs benefit from a common solution; manufacturers apply this principle in designing products and producing in volume.

An adviser developing a broadly applied investment solution for the emerging affluent’s need inventory is in keeping with this segment’s wide acceptance of portfolio models such as target date funds for retirement. The key difference is the adviser builds the solution for mass consumption with his or her own advice/counsel/wisdom—the adviser’s primary differentiating force—instead of licensing a vendor’s off-the-shelf assembly and relegating the solution to a commodity (i.e. other advisers with the same vendor package would be indistinguishable).

Technology for Mass Personalization

Technology paves the road to upholding a differentiated advisory service while also serving volumes of emerging affluent clients simultaneously.

- A proprietary “robo-adviser” instilled with the adviser’s own planning, portfolio, and investment advice that delivers the tactical solution to clients’ needs.

- Scaled communications like CRM, a portal, email, and social media that provide the service and support component necessary to keep the relationship on track.

- Periodic group meetings activate adviser-to-client relationships.

- The hand-in-glove fit here is the emerging affluent are highly accustomed to, if not preferring, these technology-based interactions.

Right-Sizing Processes to AUM Segments

Using scaled service delivery methods generates important operational leverage. The block of hours used to develop the advice and service package is distributed across many clients wherein each new client in the group further improves the profit margin of those hours. This strategic profile adds measurably to the firm’s year-over-year profits, but also its valuation, which is a winning mix by all accounts.

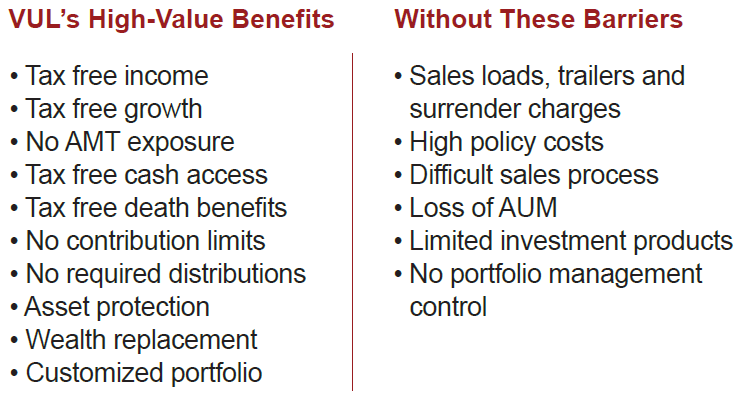

Insurance Like It Should Be: Benefits without Barriers

Advisor-Applied VUL is a vastly different – and more powerful – wealth-planning tool than your past experience may suggest. You and your clients gain VUL’s high-value benefits but the obstacles that may have prevented you from using it in the past are stripped away.

Take The Next Step.

Embrace Tax-Free Portfolios For Your HNW, High-Income Clients.

Experienced PPLI Practitioners

Investment

Products Firms

Advisors

New to AAVUL

Resources

for Advisors

Insurance Like It Should Be

Benefits, without Barriers

You’re most familiar with retail VUL and its drawbacks:

loads; high costs; complex products; investment limitations; a difficult sales process.

Check out our AAVUL partners’ solutions that keep VUL's benefits while removing the barriers.